Turkish Competition Authority Recalibrates Its Rules on Mandatory Merger Notifications

New Era for the Acquisition of ‘Technology Undertakings’ in Türkiye

Introduction

In March 2022, Turkish Competition Authority (“TCA”) introduced significant amendments to its secondary merger control legislation by disapplying the target turnover threshold for acquisitions of ‘technology undertakings’, meaning that such transactions may be notifiable even where the target’s turnover would otherwise fall below the applicable notification thresholds. The amendments mainly aimed to capture so-called ‘killer acquisitions’, as discussed in the Guidelines on the Assessment of Horizontal Mergers and Acquisitions (“Horizontal Merger Guidelines”). Also, as provided in the E-marketplace Platforms Sectoral Inquiry Final Report (“Sectoral Inquiry”) dated April 2022, the relevant amendments were implemented in lieu the then proposition that “gatekeeper platforms” should pre-notify all acquisitions regardless of the turnover thresholds to the TCA.

However, three years later after the technology undertaking exception to the notification rules entered into force, the TCA introduced a new amendment on 11 February 2026 that significantly narrowed its scope of the exception. This change is expected to restore greater prominence to the general rule of turnover-based merger notification. This development invites a closer look at how the exception has functioned in practice and whether it has effectively served its original policy objective of capturing so-called “killer acquisitions.” Throughout this piece, we aim to present an account of the implementation of the said exception and give an insight on what has changed in Turkish merger control regime.

A Summary of the Changes to the Merger Control Rules

Along with the amendments to Communiqué No. 2010/4 on Mergers and Acquisitions Requiring the Approval of the Competition Board (“Communiqué No. 2010/4”) in 2022, a new concept was introduced to the merger control regime, namely ‘technology undertakings’, which were defined as undertakings those active in the fields of digital platforms, software and game software, financial technologies, biotechnology, pharmacology, agrochemicals, and health technologies. Under the amendments, acquisitions of such undertakings did not require the target undertaking to meet the then-applicable local turnover threshold (i.e., TRY 250 million), provided that the undertaking (i) operates in the Turkish market, (ii) conducts R&D activities in Türkiye, or (iii) provides services to customers located in Türkiye.

Under the newly amended Communiqué, as of 11 February 2026, the scope of the technology undertaking exception has been significantly narrowed. Previously, the exception applied where the conditions outlined above were satisfied. Following the amendment, it now applies only to technology undertakings established in Türkiye, thereby strengthening the local nexus requirement. In addition, while the previous regime did not require the target undertaking to meet any local turnover threshold, acquisitions involving such undertakings are now notifiable only where the target’s turnover exceeds TRY 250 million, which still remains significantly lower than the new general local turnover threshold (i.e., TRY 1 billion).

Technology Undertaking Exception in Board’s Decisions

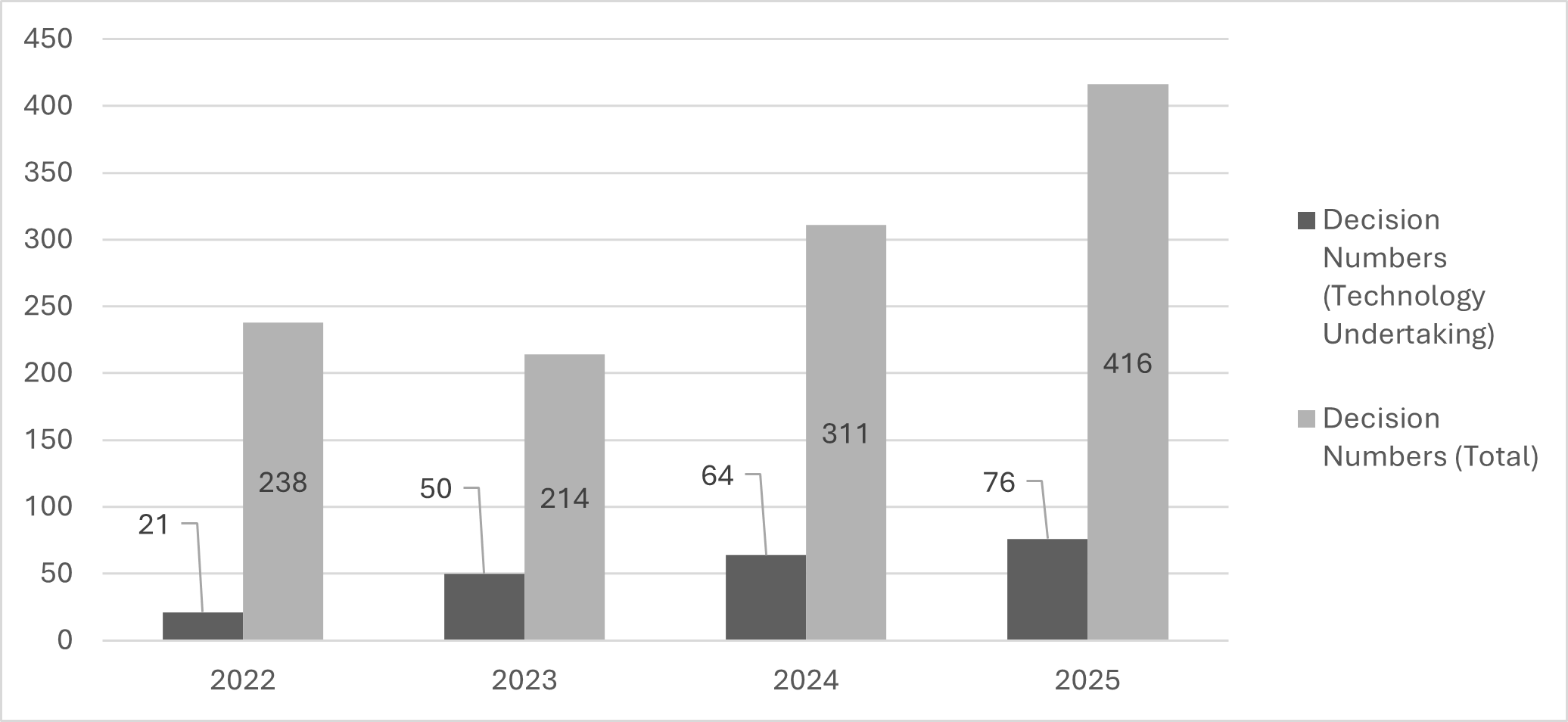

The chart below illustrates the annual distribution of TCA decisions concerning technology undertakings between 2022 (i.e., when the amended regulation entered into force), and 2025, together with the total number of merger notifications reviewed by the TCA during the same period:

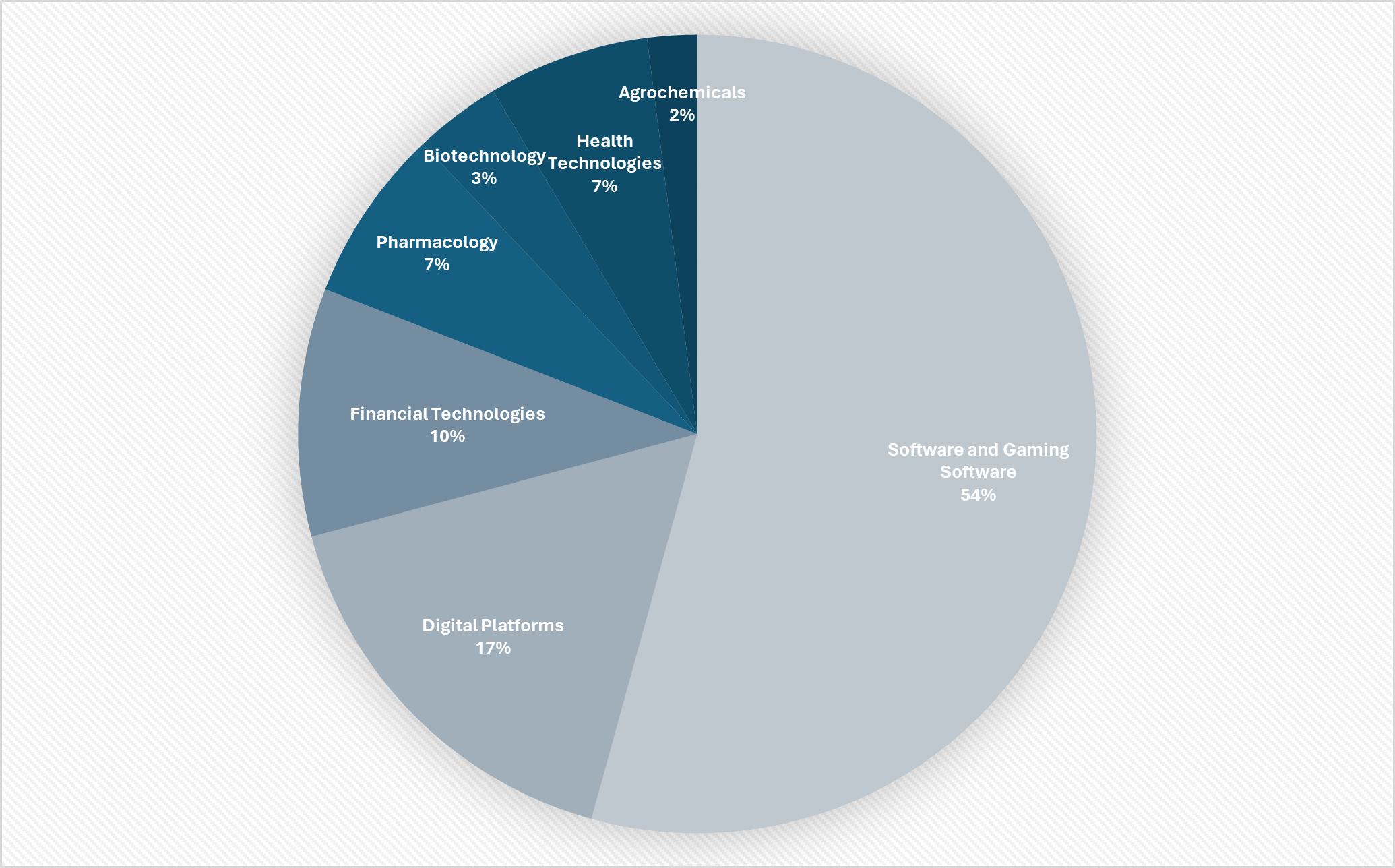

The chart below presents the distribution of TCA decisions involving technology undertakings between 2022 and 2025, broken down by the sectors in which the relevant undertakings operate.

Based on the charts above, it can be observed that a significant number of TCA decisions have involved technology undertakings, and this number has increased over the years. Notably, in 2025, approximately 18% of the TCA’s decisions concerned transactions involving technology undertakings when compared to the total number of merger control decisions issued in the same year. Moreover, as illustrated above, the majority of these decisions relate to the software and gaming software sector (54%), followed by digital platforms (17%) and financial technologies (10%). Interestingly, only one transaction notified under the technology undertaking exception involved an acquisition by an e-marketplace operator, which targeted undertakings or assets operating in the categories listed above, which was cleared unconditionally in Phase-I.[1]

That aside, the increasing number of “technology undertaking” decisions over the years is unsurprising given the TCA’s strict enforcement approach. Over these three years, the TCA applied the exception robustly in line with the notification requirements and sanctioned several undertakings in relation to transactions falling within the scope of the exception for failing to notify notifiable transactions or implementing them prior to clearance, in breach of the standstill obligation (i.e., gun‑jumping). A highly publicised decision was a gun-jumping fine with respect to Elon Musk’s acquisition of Twitter Inc. in 2023.[2] Another decision was a fining decision regarding Param’s (a financial services company) acquisition of Kartek due to the violation of standstill obligation in 2024.[3] Again, the TCA applied gun jumping fine on Broadcom relating to its pre-mature acquisition of VMware based on the newly introduced technology undertaking exception under the Communiqué No. 2010/4.[4]

Substantive Review of “Killer Acquisitions”

Over the years, an overwhelming number of transactions which were notified under the technology undertaking exception were cleared in Phase-I, while very few number of transactions were subject to an in-depth review by the TCA (i.e., Phase II). We have found four decisions in total, which explicitly referred to “killer acquisitions” while assessing these transactions in substance. Notably, all four decisions concerned acquisitions of technology undertakings and were ultimately cleared by the TCA in Phase-I without further in-depth review.

In TCA’s decision relating to Galileo AI Inc.’s acquisition by Google[5], the TCA concluded that a typical “killer acquisition” occurs where the following conditions are cumulatively met: (i) there must be an acquisition of a newly established or developing undertaking by a large, established undertaking; (ii) the acquired product or technology should be neglected or completely withdrawn from the market; and (iii) competition should be eliminated at horizontal level and product‑development processes should be terminated. The TCA cleared the relevant transaction based on the findings that (i) Galileo did not operate as the AI technology supplier and their activities did not horizontally overlap in this sense and (ii) Galileo had significant competitors in the market such as Adobe XD and Figma Design.

In a subsequent review of “killer acquisitions” related to the acquisition of Pixelmator by Apple[6], the TCA recognised that the acquisitions of newly established or developing undertakings by a large, established undertaking could lead to potential competitive harms (i.e. killer acquisitions), on the other hand, it could also lead to competitive outcomes by incentivising innovation. The TCA conducted a thorough analysis of potential vertical/horizontal anti-competitive effects and found that no appreciable anti-competitive effect arose from the transaction. However, in a dissenting opinion to the decision, a member of the Board posed that a routine analysis of vertical/horizontal effects was insufficient for the purpose of the assessment of the merger in question; and a counterfactual analysis of the transaction should have been made in light of the killer acquisition theory of harm, also taking into account the ecosystem that Apple operated.

In a third decision regarding the acquisition of NEF (operating in the design, development, marketing, and distribution of digital platforms that provide financial analysis and financial document, table, and record auditing services) by Mikro[7], the TCA assessed that there are many competitors and no high barriers to entry in the market where NEF operates. Therefore, it found that the relevant transaction would contribute to strengthening the existing competition and innovation on the market.

Lastly, regarding Take-Two’s acquisition of Gybe Games/Color Block Jam (a mobile video game)[8], although the TCA did not conduct an in‑depth review, this approach was criticized in a dissenting opinion by a Board member. The dissent argued that, given the oligopolistic structure of console gaming, ongoing vertical integration trends, and the fact that two operating systems act as gatekeepers of the mobile ecosystem, independent (indie) games represent the only genuine avenue for market entry. Therefore, a deeper/broader analysis and a market review should have been made based on new theories of harm instead of simply conducting traditional vertical/horizontal effects analyses within the scope of the review.

On other decisions, the TCA did not make reference to killer acquisitions, it conducted an in-depth review of horizontal/vertical/conglomerate effects, while clearing these transactions in Phase-I due to lack of appreciable anti-competitive effects on the relevant markets.[9]

Conclusion and Key Takeaways

TCA has been a rigorous enforcer to review the acquisitions in the technology space over the years. However, it has adopted a rather tolerant approach regarding the substantive evaluation of these transactions, despite dissenting voices underscoring the importance of adopting new theories of harm such as killer acquisitions and ecosystem harm theories. That said, the recent amendments to the technology undertaking exception appear to align with the TCA’s relatively tolerant approach to substantive analysis, as they may help avoid unnecessary bureaucracy and support facilitating foreign investments, also considering the Authority’s busy agenda.

Given that the TCA did not abolish the technology undertaking exception altogether, it is clear that the Authority intends to remain active in reviewing acquisitions of technology undertakings, albeit to a more limited extent. From this perspective, while the decision to review acquisitions of technology undertakings that already generate a certain level of turnover appears reasonable, it is also important to note that the new rule may come at the expense of missing acquisitions involving nascent technologies and early-stage start-ups. Therefore, it would not be surprising to see fewer TCA decisions referring to the theory of killer acquisitions in the future. In this context, it may also be debated whether the introduction of an acquirer-based notification rule, similar to the approach reflected in the Horizontal Merger Guidelines and previously discussed in relation to gatekeeper platforms, could once again become a hot topic in Türkiye.

[1] TCA’s decision dated 03.08.2023 and numbered 23-36/672-228.

[2] Elon Musk/Twitter, TCA’s decision dated 02.03.2023 and numbered 23-12/197-66. See also. https://www.rekabet.gov.tr/en/Guncel/the-examination-about-the-acquisition-of-d384a31c4ebfed118eb0005056850339

[3] Kartek/Param, TCA’s decision dated 04.04.2024 and numbered 24-16/390-148.

[4] VMware/Broadcom, TCA’s decision dated 18.07.2024 and numbered 24-30/707-296. For the other decisions see: AutoAttack Games Ltd / Modern Times Group decision dated 25.09.2025 and numbered 25-36/858-506; Plarium Global Ltd. /Modern Times Group decision dated 25.09.2025 and numbered 25-36/856-504; Snowprint Studios AB / Modern Times Group decision dated 25.09.2025 and numbered 25-36/857-505.

[5] Galileo/Google, TCA’s decision dated 16.01.2025 and numbered 25-02/62-37.

[6] Pixelmator/Apple, TCA’s decision dated 06.02.2025 and numbered 25-04/99-56.

[7] NEF/Mikro, TCA’s decision dated 25.9.2025 and numbered 25-36/864-510.

[8] Gybe/Take-Two, TCA’s decision dated 31.07.2025 and numbered 25-28/665-403.

[9] See e.g. Google/Photomath, TCA’s decision dated 28.04.2023 and numbered 23-19/354-121; Activision/Blizzard, TCA’s decision dated 13.07.2023 and numbered 23-31/592-202; Synopsys/Ansys; TCA’s decision dated 06.03.2025 and numbered 25-09/202-103.